Want to hear it straight from the speakers? Watch the full discussion at the end of the article.

The industry is growing, but not equally everywhere

Despite a tougher macro environment, business aviation activity continued to grow. WINGX reported total growth of 4.6 percent YTD in 2026 versus 2025. Regionally, growth was strongest in South America at 8.2 percent, followed by the United States at 5.3 percent, Europe at 3.6 percent, and Asia at 3.3 percent.

But headline activity only tells part of the story.

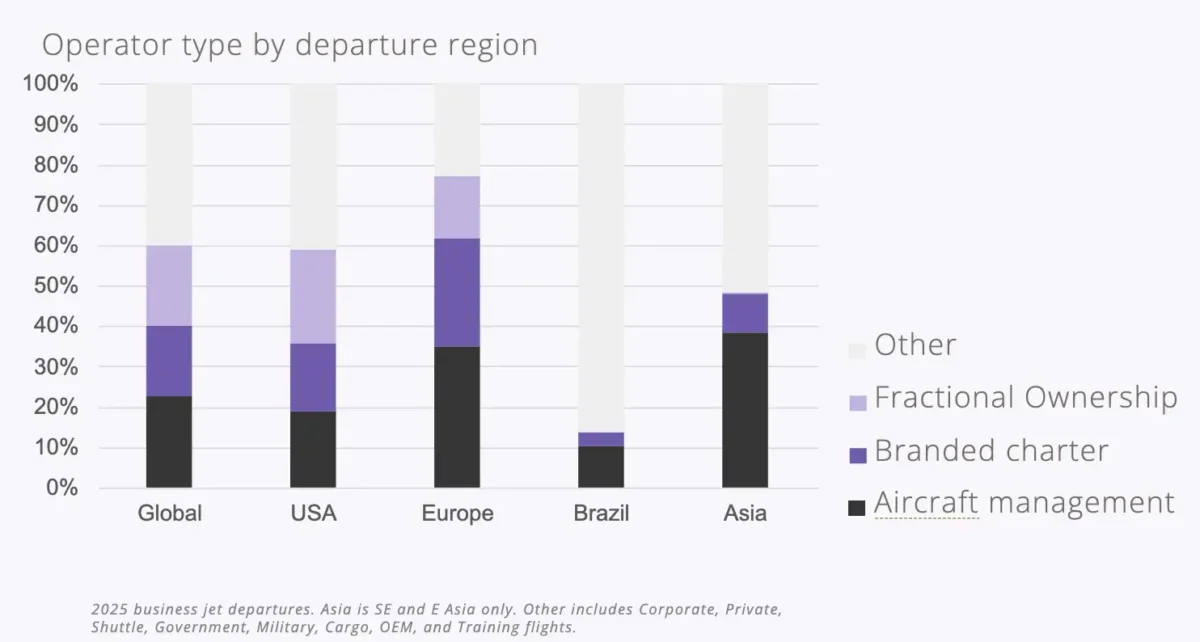

Each region is built on a different operator mix. Corporate and private flying dominate in Brazil, while branded charter and aircraft management are the backbone of Europe.

That matters because regional growth does not automatically translate into open charter opportunity. The same commercial strategy will not work everywhere.

As Richard Koe put it: “We are in a solid place as an industry, which is interesting because that is somewhat decoupled from a pretty nasty macro environment.

Source: WINGX.

The bigger opportunity is increasingly cross-border.

The transatlantic corridor remains the most valuable inter-regional charter market, worth $1.27 billion and up 79 percent since 2019. Regional strength at home is no longer enough.

North America still dominates overall business aviation activity, accounting for roughly 70 percent of movement. Europe, however, generates a much larger share of charter value than its movements alone suggest, representing only around 12 percent of total movements but roughly 30 percent of the total charter market value.

That gap is driven by a different demand profile: more charter activity, longer-range flights, larger aircraft, and higher-value international routes.

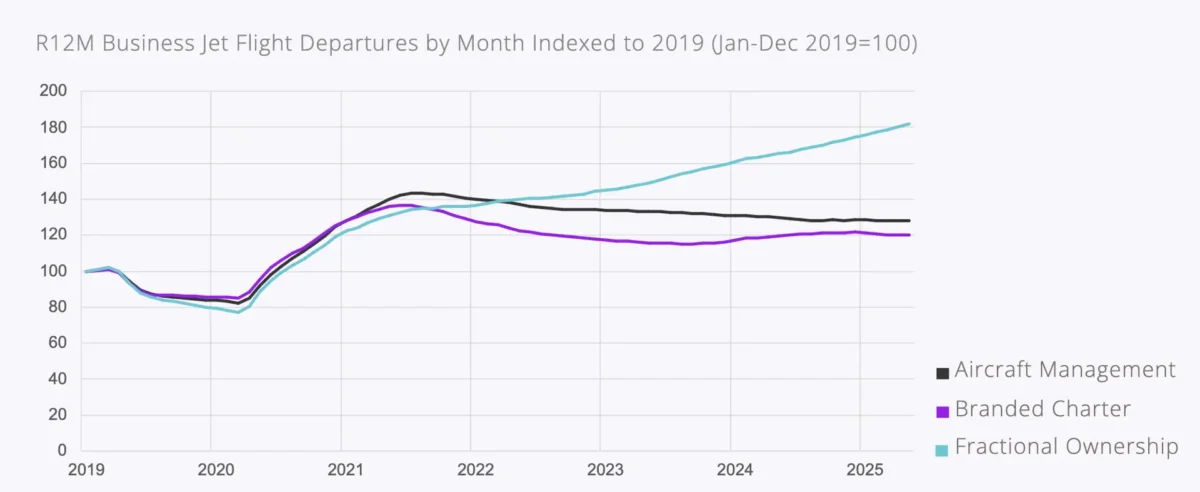

Fractional is changing what growth actually means

A growing market does not automatically mean a bigger open charter market.

While demand continues growing, business aviation itself is starting to look very different from what it did a few years ago. A big reason for that is the rise of fractional ownership.

WINGX data shows the fractional fleet has grown by 50 percent since 2019 and now generates the largest share of flight activity, despite representing only 7 percent of aircraft in the market.

As more demand stays inside closed fractional programs, fewer trips reach the open charter market. For operators and brokers, that changes the competitive landscape. Growth is still there, but it is not always accessible through the same channels.

Source: WINGX.

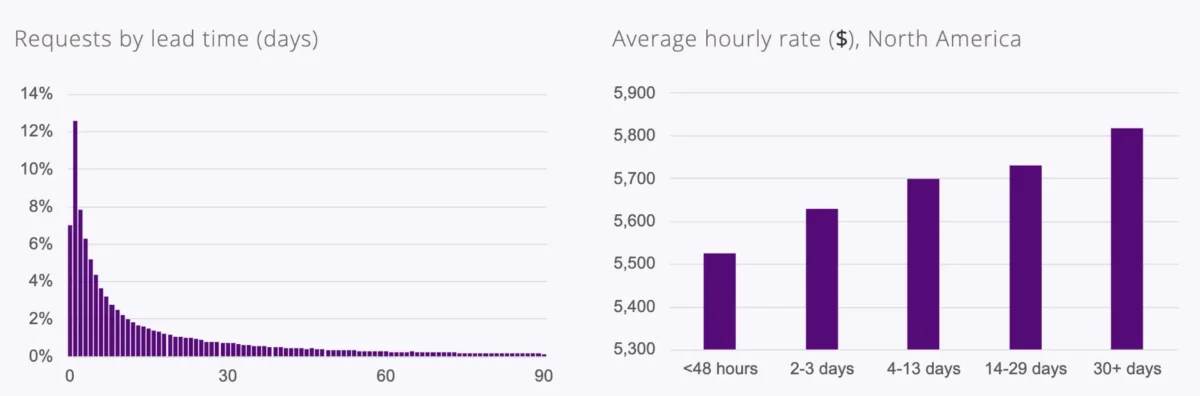

Booking behavior is faster, later, and harder to price

The changes are also becoming visible in how customers book charter.

Avinode data shows a market that has become far more last-minute, with most requests now coming in only a few days before departure. Unlike commercial airlines, prices often decrease closer to departure rather than increase.

Pricing itself has changed a lot since the pandemic. Rates have stayed higher overall, but they have also become much less predictable. Busy travel periods now create sharper swings, while rising fuel, maintenance, and operating costs continue to put pressure on margins.

That makes pricing much harder to get right.

Operators now need to react much faster to changes in demand, availability, and costs. In a market moving this quickly, relying on flat pricing or slower decisions can easily leave revenue behind, which is why the operators performing best are often the ones adjusting fastest to what the market is telling them.

As Oliver King said, operators who have not addressed this are “missing money on the table.”

Richard Koe summed up the opportunity: “The data is there to predict where that aircraft needs to be, what kind of aircraft it needs to be, and what route it’s likely to fly.”

The FIFA World Cup is a $500 million opportunity

In a market driven by shorter booking windows and faster-moving demand, being able to prepare ahead of time becomes a major advantage.

The upcoming FIFA World Cup 2026 is a good example of that.

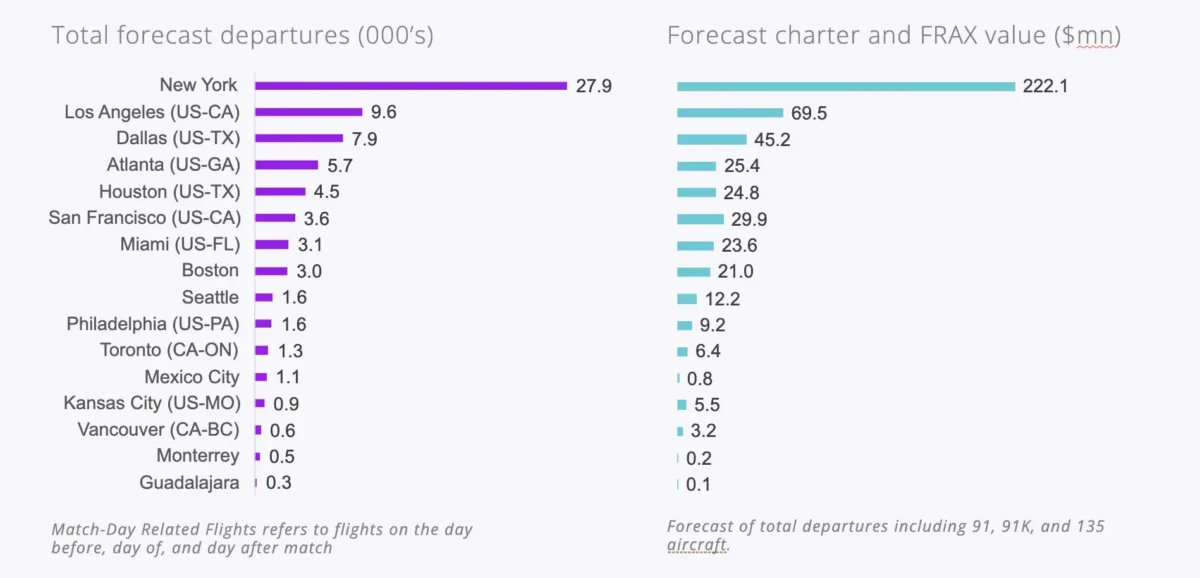

Previous tournaments show how sharply traffic can spike around match days. WINGX data shows group-stage matches roughly doubled business jet activity, while finals generated surges of up to 23 times normal levels.

For 2026, WINGX forecasts around $500 million in charter and fractional value across North American host cities, with a significant share expected to come directly from tournament-related demand.

The opportunity will not be evenly spread. New York alone is forecast to generate $222 million in charter and fractional value, followed by Los Angeles at $69.5 million and Dallas at $45.2 million.

The operators and brokers who benefit most will be the ones that understand demand patterns early, position aircraft ahead of time, and prepare for how traffic is likely to move as the tournament progresses.

As Oliver put it: “There is a cake, and now is the time to plan for your slice.”

The data-driven future of charter

Across the Avinode and WINGX data, one message stands out: the operators and brokers staying closest to demand are the ones staying ahead.

From pricing and aircraft positioning to understanding booking patterns and traffic flows, data is becoming a much bigger part of how charter works day to day. The information is already there. The challenge is knowing how to act on it quickly enough.

As charter becomes more competitive, operators and brokers that rely on slow decisions, static pricing, or familiar markets will fall behind. The companies most likely to grow are the ones using data to move earlier, price smarter, and look beyond their usual demand base.

Node Talks is Avinode’s members-only event for business aviation, bringing the industry together for high-value networking and focused conversations on the market’s most important topics.