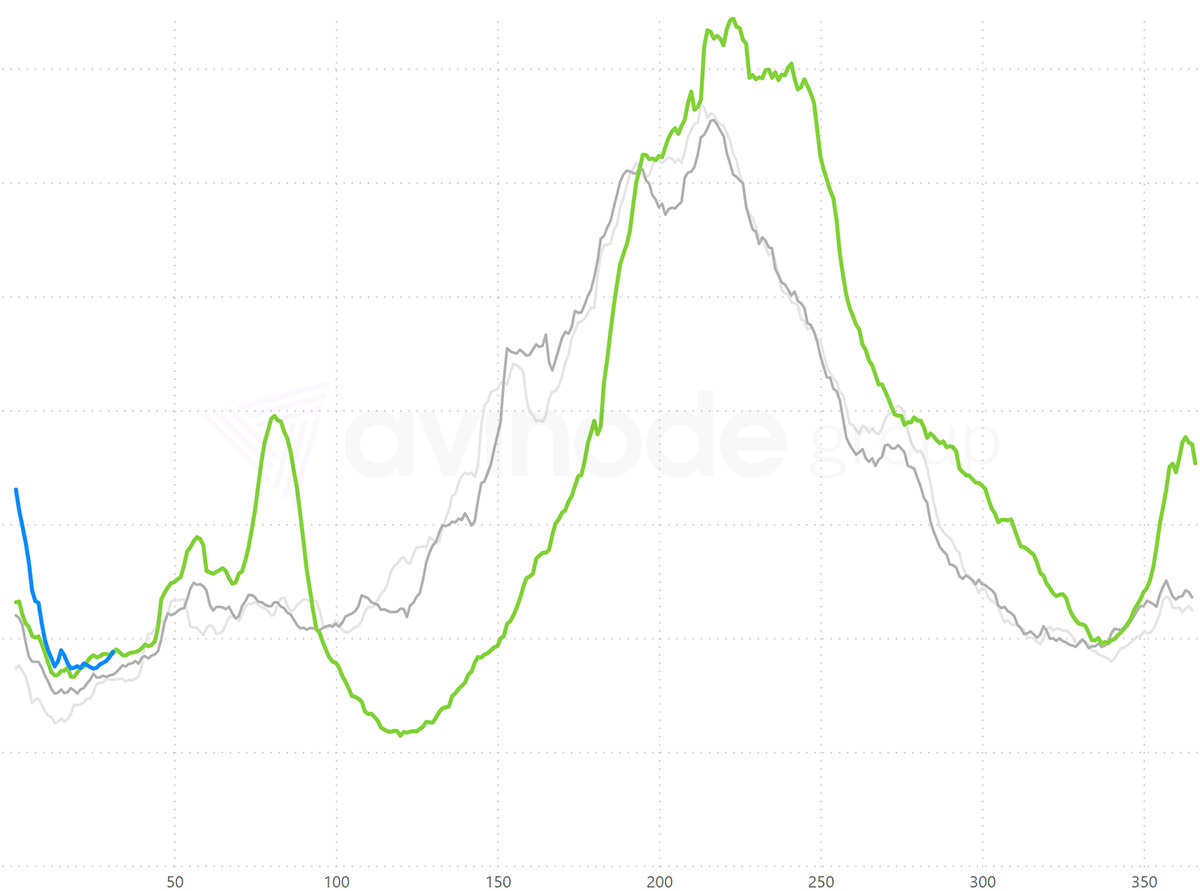

Intra-European demand

The charts below are rolling 14-day indexes of demand for trips requested through the Avinode marketplace within the regions specified. Each chart shows relative demand within the region for 2021 in blue, 2020 in green, 2019 in dark grey and 2018 in light grey, with day of year along the horizontal axis. Being indexes, the exact figures on the vertical axis are not relevant, although it is worth noting that the axes do start at zero.

Right now, Intra-European charter demand through Avinode is not too different to previous years. This statement conceals some large year-on-year changes. Smaller categories are more resilient than heavier categories and geographically, the recovery is uneven.

“Demand between European countries shifted rapidly due to restrictions in 2020 and that pattern looks set to continue in 2021.”

Lockdowns, Brexit and a lack of skiing mean that the worst year-over-year statistics are for travel from the UK and Switzerland. Charter demand out of Spain has been up at the start of the year and looks set to remain so for at least the next two weeks, driven by travel to the UK and Germany. Portugal is also seeing some very spikey demand to the UK in relation to restrictions on travel from there. Demand between European countries shifted rapidly due to restrictions in 2020 and that pattern looks set to continue in 2021.

Over the winter, travel rules within Europe have seen demand pick up to longer-haul destinations – the UAE, Maldives, and Caribbean islands. Broadly, those trends continue. Demand to the UAE is consistently elevated all the way until Easter whilst the Maldives is spiking on February weekends. The Bahamas and Barbados look to be taking early demand for Easter from Western Europe, whilst Zanzibar is popular for the next couple of weeks from Eastern Europe.

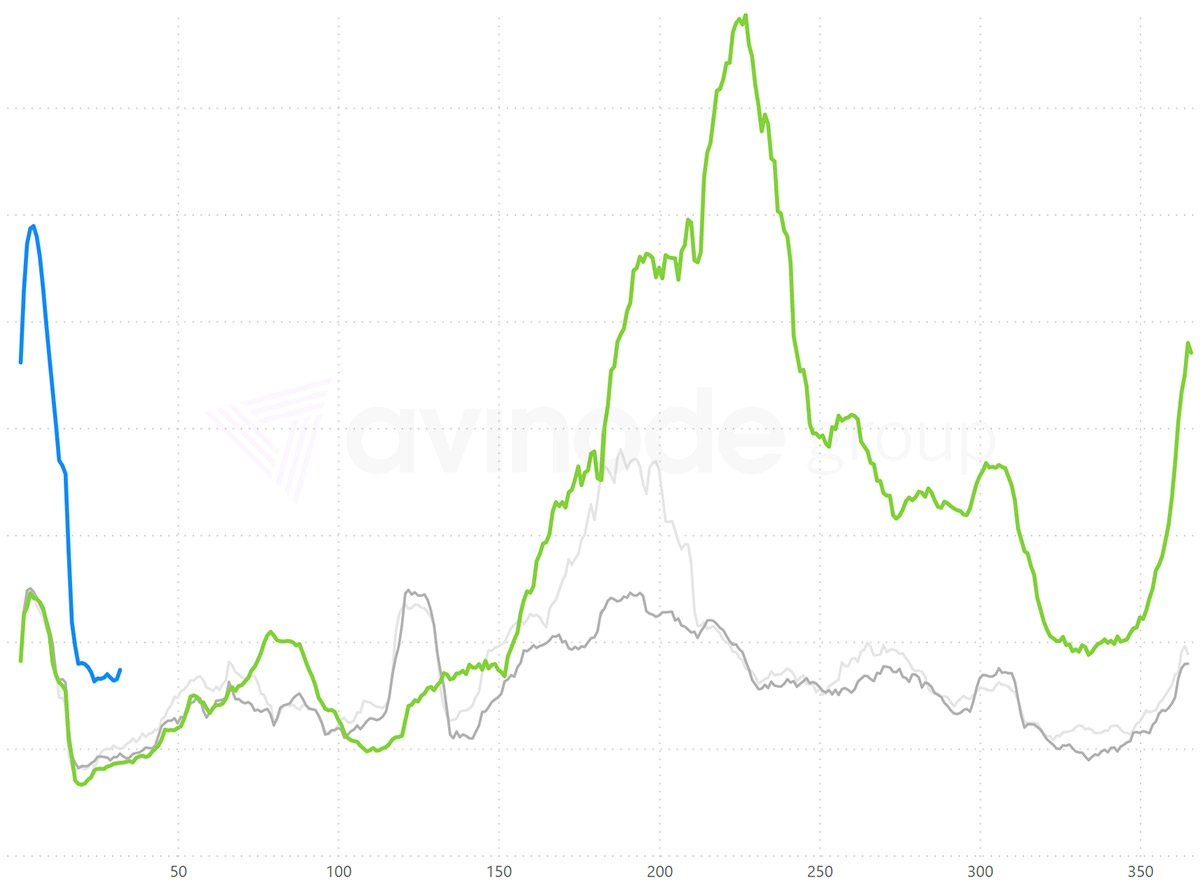

Demand from Russia & CIS

In the second half of 2020, charter demand from Russia & CIS grew considerably in Avinode and that pattern has remained in 2021. The main drivers have been domestic travel within Russia (Sochi to Moscow #1), trips to the UAE and the Maldives. Whilst it is too early to comment on long term domestic demand changes, the data for early Q2 suggests that demand to these sunspots will continue into April.

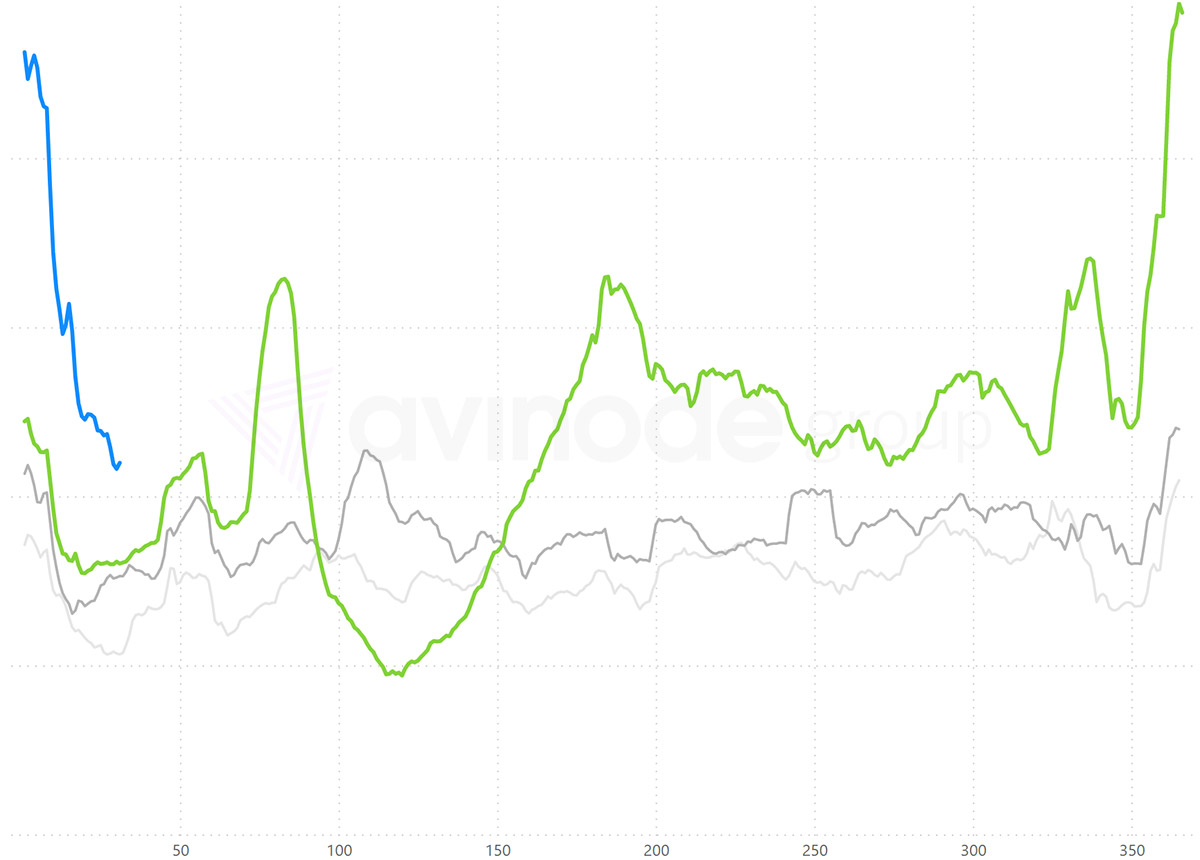

Domestic demand within the USA

Travel within the United States through the Autumn and Winter has been far more resilient than in Europe. We saw record demand through Avinode during the Thanksgiving and Christmas holiday period, likely driven by an influx of new leisure customers to the charter market in 2020.

Looking forward, demand curves for US domestic travel are slightly ahead of last year’s level for the next 3 weeks. The flows showing positive year-over-year trends are those that did OK in 2020 – primarily travel to and from Florida. Aspen and Salt Lake City look like popular arrival points for some Valentine’s Weekend snow. Hawaii is consistently more popular than last year. Demand for short flights is having a tougher time; demand within California is down 56% for the next 4 weeks. Demand within the Northeast of the country is similarly depressed.

Global trends and indications

Looking north of the border, Canadian demand through Avinode has pivoted away from domestic and US travel and is focused firmly on trips to the Caribbean for the next couple of months. The Turks & Caicos and Sint Maarten are popular from both Canada and the USA, which is also seeing year-over-year demand increases to Puerto Rico, the US Virgin Islands and Costa Rica.

Elsewhere in the world, demand in Q1 from the Middle East is being driven by the previously highlighted trends from Dubai to Europe & Russia. Demand for travel within the Middle East is broadly down, except for Qatar. A wide range of African countries that saw minimal demand this time last year are seeing requests for charter – highlighting the continued role that business aviation must play in a world of heavily reduced commercial airline schedules.

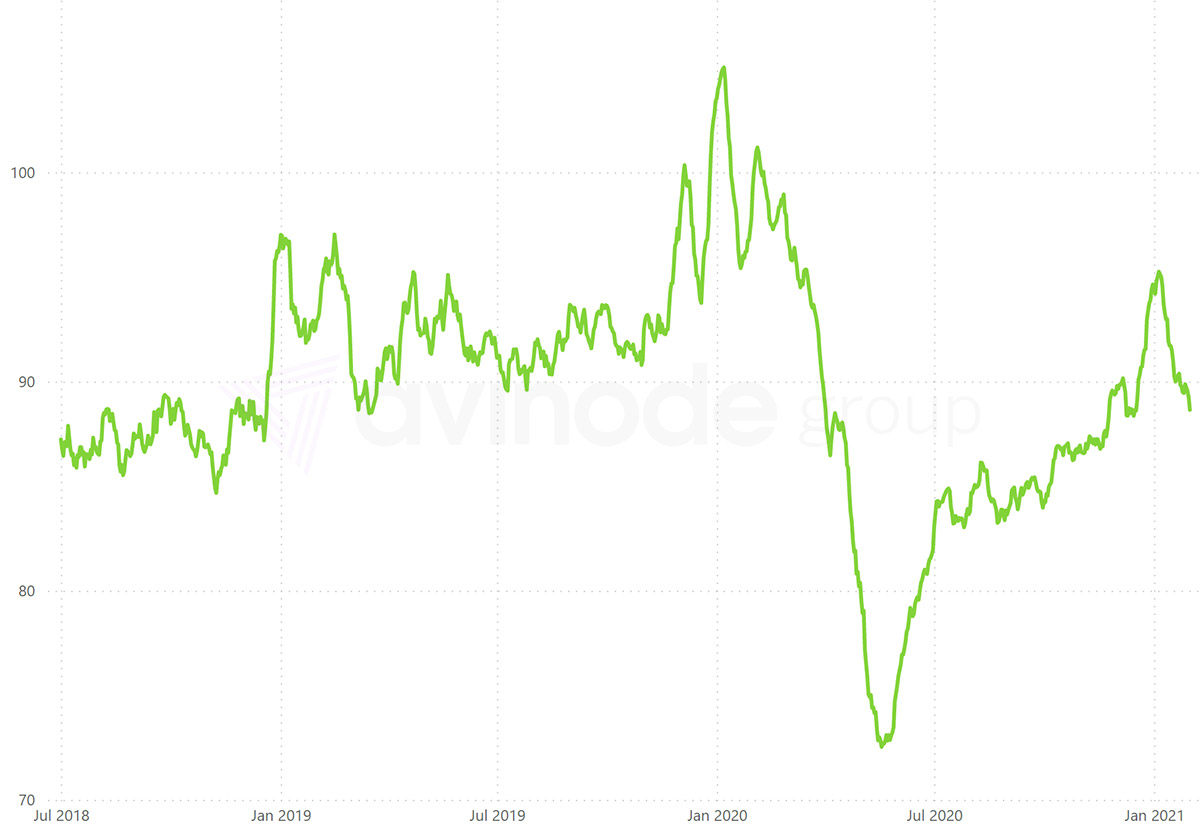

Pricing index for intra-European trips

Charter rates have adjusted to reflect the shifting demand environment. The above chart is a rolling 14-day price index based on quotes in the Avinode marketplace, normalised to 1st January 2018, for travel within Europe. Since the pandemic struck, we have seen a couple of rate decreases and recoveries. Rates are now trending down again, after a relatively positive Christmas.

Pricing index for US domestic trips

In the United States, the drop in hourly rates during the immediate aftermath of travel restrictions was greater – and the recovery has been more sustained. Rates peaked over Christmas but have started to trend down again as we have got deeper into January. However, the Autumn suggests that if demand recovers, rates should follow.

Another year of fluctuations?

In many ways, private charter has been a relative bright spot in terms of industry recovery globally – although it is an uneven recovery that has not yet got back to where it was. Back in 2020, vaccine “passports” were often suggested as being the solution to seamless travel in a pandemic world. However, countries that are winning the race to vaccinate, like Israel and the UK, are desperate to avoid new strains entering their territory. How much international travel opens from these nations depends on the severity of return quarantine measures implemented – and right now, it does not feel like anyone could confidently say what these will be in the long term.

2020 was a year of fluctuations; expect more of the same in 2021.

Harry Clarke,

Head of Insight, Avinode Group